Feeling overwhelmed by your finances? You’re not alone. Many people struggle to strike a balance between essential spending, enjoying life’s little pleasures, and saving for the future. That’s where the 50/30/20 rule comes in – a simple yet powerful budgeting framework that can help you take control of your money.

What is the 50/30/20 Rule?

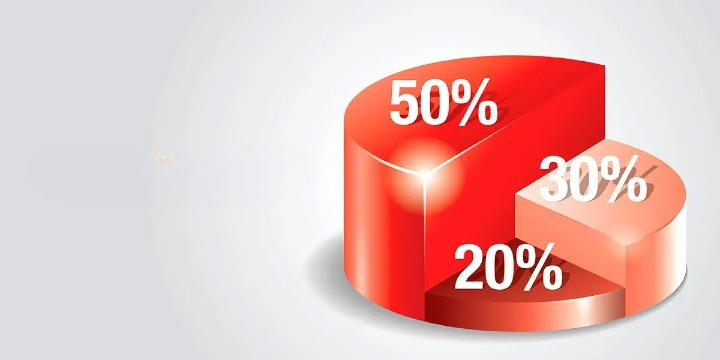

The 50/30/20 rule is a straightforward budgeting strategy that divides your after-tax income into three categories:

- Needs (50%): These are essential expenses you can’t live without, such as rent/mortgage, utilities, groceries, transportation, and minimum debt payments.

- Wants (30%): This category covers discretionary spending – things you enjoy but aren’t necessities. Examples include dining out, entertainment, hobbies, subscriptions, and vacations.

- Savings & Debt Repayment (20%): This crucial pot is dedicated to building your financial safety net and chipping away at debt (excluding minimum payments). It includes emergency savings, retirement contributions, and additional debt payments.

Why is the 50/30/20 Rule Effective?

The beauty of the 50/30/20 rule lies in its simplicity and flexibility. It provides a clear structure for allocating your income, ensuring you prioritize essential needs while leaving room for financial goals and a bit of fun.

Here are some key benefits:

- Prioritizes Necessities: By allocating half your income to needs, you’re less likely to fall behind on essential bills.

- Promotes Financial Wellbeing: The focus on savings allows you to build an emergency fund, plan for retirement, and achieve long-term financial goals.

- Allows for Discretionary Spending: The 30% allocated for wants ensures you can still enjoy life’s pleasures without derailing your financial progress.

- Easy to Understand and Implement: The clear percentage breakdown makes it easy to grasp and adapt to your specific situation.

Also Read: Adjustment to EF ATM Deposit: Understanding the Term

Adapting the 50/30/20 Rule to Your Needs

Remember, the 50/30/20 rule is a guideline, not a rigid formula. Here’s how you can personalize it:

- Adjust the Percentages: For example, if your housing costs are high, you might need to allocate slightly more than 50% to needs. Conversely, if you’re debt-free and have a high income, you could increase savings beyond 20%.

- Track Your Spending: Monitor your expenses for a month to understand where your money goes. This will help you identify areas for adjustment within each category.

- Automate Savings: Set up automatic transfers to savings or retirement accounts. This ensures consistent saving and removes temptation.

Beyond the 50/30/20 Rule: Building a Strong Financial Foundation

While the 50/30/20 rule is a great starting point, consider these additional tips for a well-rounded financial strategy:

- Set SMART Financial Goals: Having specific, measurable, achievable, relevant, and time-bound goals keeps you motivated and focused.

- Learn About Different Investment Options: Explore investment opportunities like IRAs or mutual funds to grow your wealth for long-term goals.

- Seek Professional Help: Consulting a financial advisor can provide personalized guidance based on your unique circumstances.

The 50/30/20 rule empowers you to take charge of your finances. By following this framework and incorporating additional strategies, you can build a secure financial future and achieve your financial goals with confidence.